Philippine SeaBank's Time Deposit Auto Renew Feature

I designed SeaBank Time Deposit Auto Renew, helping users keep saving without redoing the deposit flow. This case covers how I integrated Auto Renew into an existing journey, balancing clarity, user control, and retention. Post-launch, adoption hit 22% and 72-hour drop-off fell from 44% to 27%.

Role

Product Designer

Timeline

6 months (Jun - Dec 2025)

What I Worked On

Design exploration & prototyping, cross-functional collaboration, final design delivery and UAT

Teams Involved

Product Manager, Product Designer, Engineers, Data, Local CS/Ops, Compliance Team, Business

SeaBank: helping millions build better financial habits

SeaBank is a digital bank in the Philippines, part of Monee, formerly SeaMoney, the financial services arm of Sea Group. With a mission to expand access to mobile banking across Southeast Asia, SeaBank supports everyday savers and underbanked users with simple, mobile-first financial tools.

What's the problem?

While many users redeposit their funds upon maturity, they have no efficient way to do so. This creates a post-maturity gap in which some funds go idle or leave the bank, leading to AUM leakage.

So, the challenge becomes...

How might we help users to easily set up continuous savings without disrupting their familiar flow and simultaneously minimizing AUM leakage?

and... what's the outcome

Outcome

I delivered a clear, user-controlled Auto Renew experience for SeaBank Philippines Time Deposits, so users can continue saving at maturity without redoing the deposit flow. The solution reduced post-maturity drop-off, reached the targeted adoption rate, and improved retained principal, supporting stronger long-term savings behavior and AUM retention.

Problem Validation

To validate the problem, I partnered with the Local Ops and Data teams to analyze 6 months of deposit behaviors, and we uncovered…

56%

of Time Deposit users choose to redeposit

This means there's almost half of the funds enter the leakage window.

82%

of those redeposited money have the same tenure with the previous one

Suggesting that flow repetition is redundant for loyal users.

14 days

of average "idle" duration

Users who eventually reinvest their deposit upon maturity indicate that the barrier is not "lack of money," but "lack of attention."

Business Goal

Every non-renewed deposit represents AUM (Assets Under Management) Leakage. By failing to capture intent at the moment of maturity, the bank loses liquidity to competitors.

Want a way to stop the risk of losing millions in AUM.

Every non-renewed deposit represents AUM (Assets Under Management) Leakage. By failing to capture intent at the moment of maturity, the bank loses liquidity to competitors.

Choosing the right feature

After we had a full understanding of users' problems and business goal, the first step we took to find a solution was to explore some feasible features.

1st Feature Exploration:

Notification + Shortcut

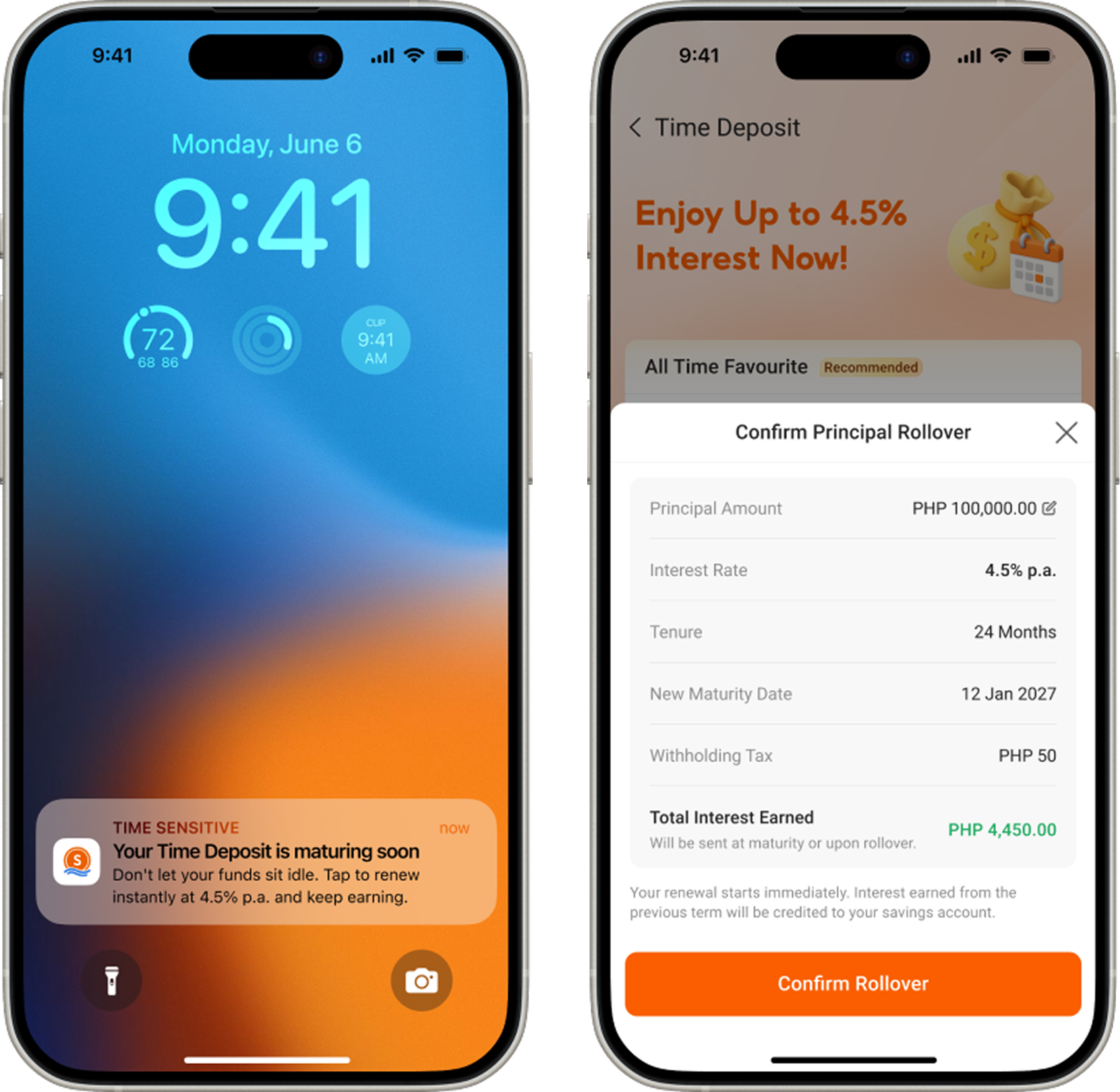

A notification will be sent 3 days before the maturity day and on the maturity day. The flow will be User taps Notification → Deep-links to a "Rollover?" Bottomsheet → User confirms (skipping the placement form).

2nd Feature Exploration:

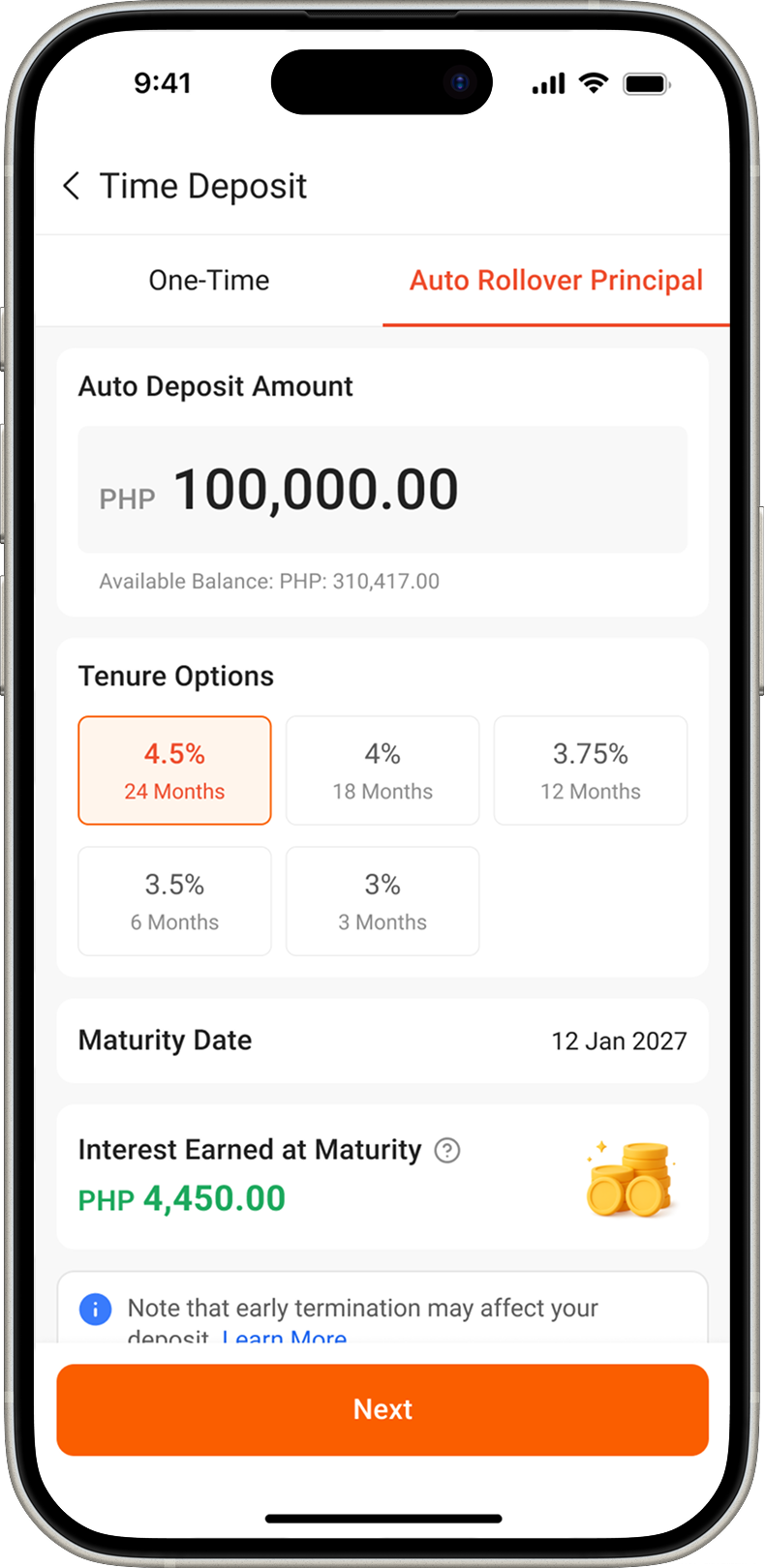

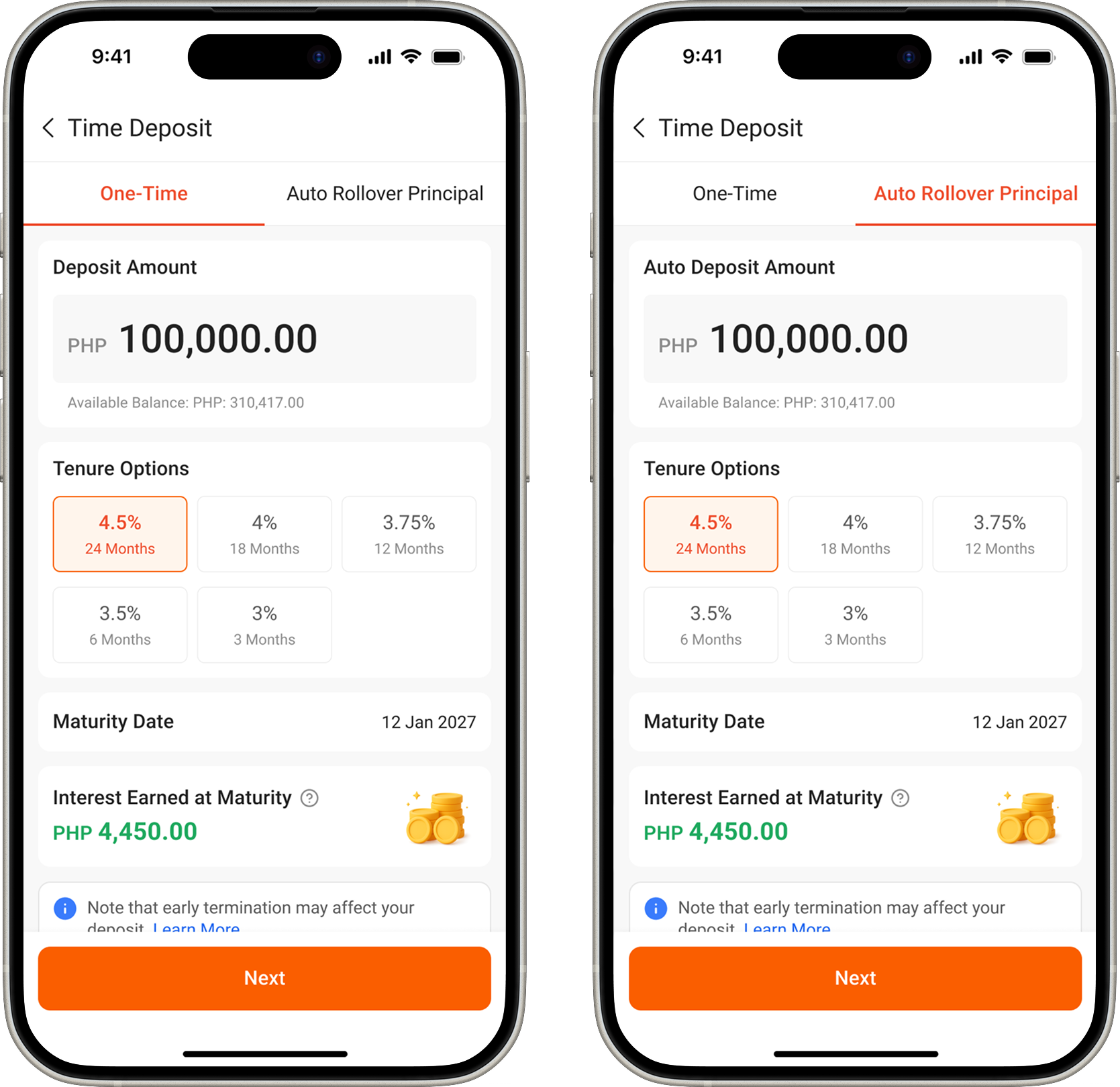

Adding Auto Rollover Setting in the Deposit Placement Flow

Add a new section in the placement flow to capture the renewal preference during the initial deposit placement.

and... the decision was...

✅ We chose Rollover Setting in the Deposit Flow

The reason is because it captures the decision proactively when users are already motivated, delivers high reliability once set, and requires no ongoing user attention, which eliminates the post-maturity gap and AUM leakage risk. The added step introduces only moderate friction, and we mitigated it with clear, reassuring UX.

Competitor Analysis

To deepen our understanding of the Auto Rollover feature, I partnered with local market research teams to evaluate Time Deposit auto-rollover features across top 6 banks in the Philippines.

"Zero-Guidance" Friction

Competitors present neutral options that force users to calculate trade-offs on their own, triggering Decision Paralysis and leading them to pick the manual default to stay safe.

Difficult mid-term changes

The majority of the apps hide their rollover instructions behind account details and are limited by cutoff windows near maturity.

Hidden maturity status

Rollover and maturity details are buried in account pages, with no clear countdown or visibility.

Design Principles

To guide our design decisions while keeping all stakeholders aligned, we defined our design principles. This ensures the auto-rollover feature feels intentional and natural.

User Control

Users must be able to review, adjust, or opt out with confidence.

Clear & Transparent

We prioritize Meaningful Friction, ensuring every rollover is an intentional, high-confidence choice.

Prevent Drop-offs

Design should remove friction that causes users to quit mid-flow.

Familiar by Default

Auto-rollover should feel natural, not like a new behavior.

Success Metrics

25%

Auto-Rollover Adoption

Measures user trust and willingness to proactively keep funds invested.

<30%

Post-Maturity Drop-Off (72H)

Indicates reduced idle balances and short-term AUM leakage immediately after maturity.

+8-12%

Portfolio Retention Volume

Shows sustained capital retention over time, beyond short-term feature usage.

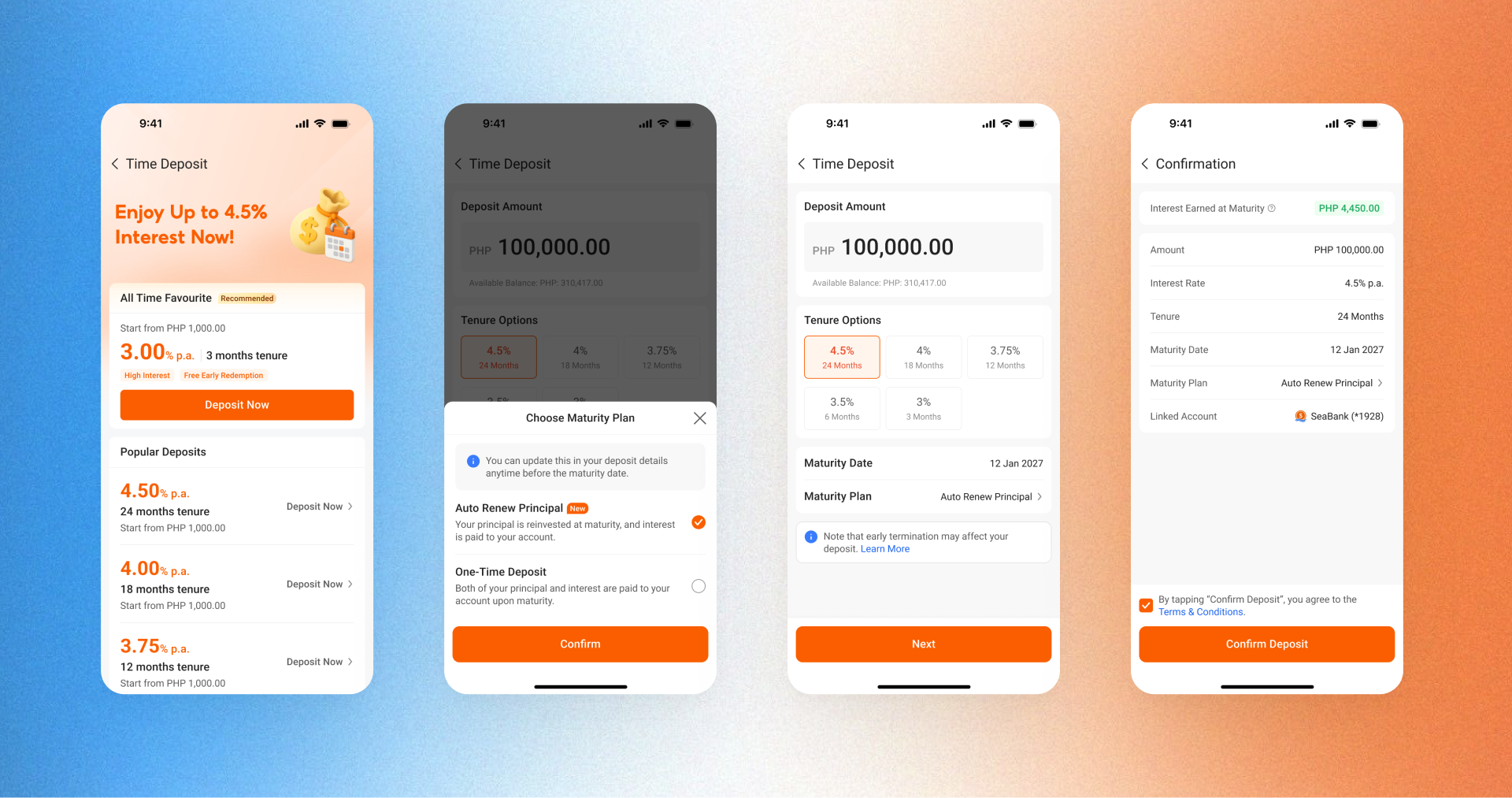

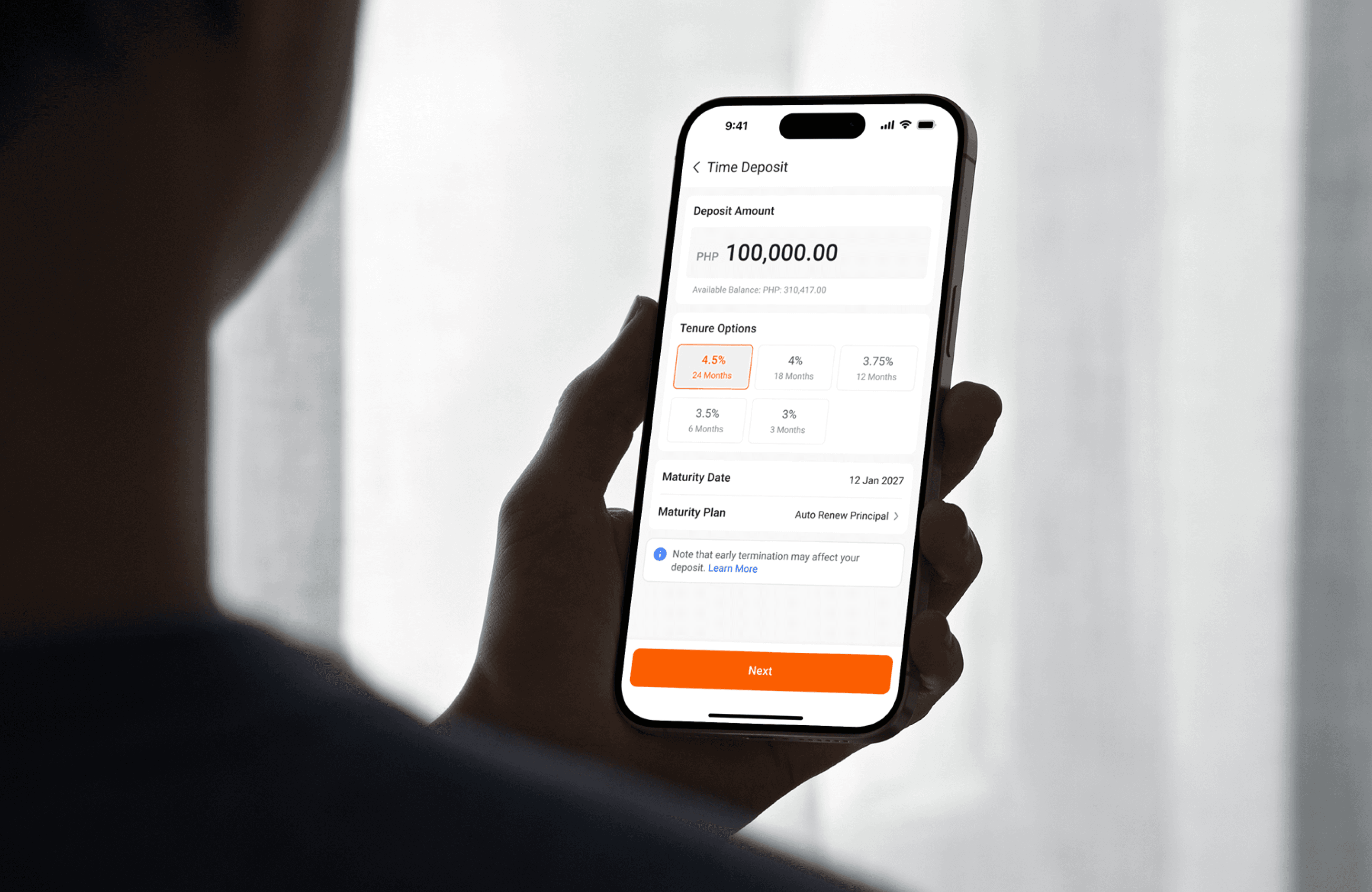

Design Exploration: Part 1

Setting The Right Flow

When I started the design explorations, I had this one critical question: When is the right moment to ask users to decide on rollover options?

We started with...

Auto Rollover After Deposit Placement

We approach this idea because it wouldn't interrupt the existing flow. But, it hid the feature at the very end, felt like an extra step, and may cause low opt-in.

So we tried...

Asking Before Deposit Placement

We approach this idea to maximize visibility and lock in intent early. But it forced a decision too soon, raised cognitive load, and risked drop-off.

Finally, we went with...

Asking Inside The Placement Page

It's the best balance because users decide with full context, with minimal disruption. Although it adds one more choice, clear copy and confirmation kept it safe and easy.

Design Exploration: Part 2

Choosing The Best Way to Display Rollover Options

After all stakeholders were aligned on the direction of the flow, I had another question: What is the best way to display it on the placement page?

Option 1:

Tab

We explored tabs to maximize visibility and make switching effortless. Placing it below the top bar keeps the choice front and center, so users can compare options at a glance.

Option 2:

Switch Toggle

We explored a toggle to keep friction near-zero. It's familiar, thumb-friendly, and visually minimal, which helps protect placement conversion.

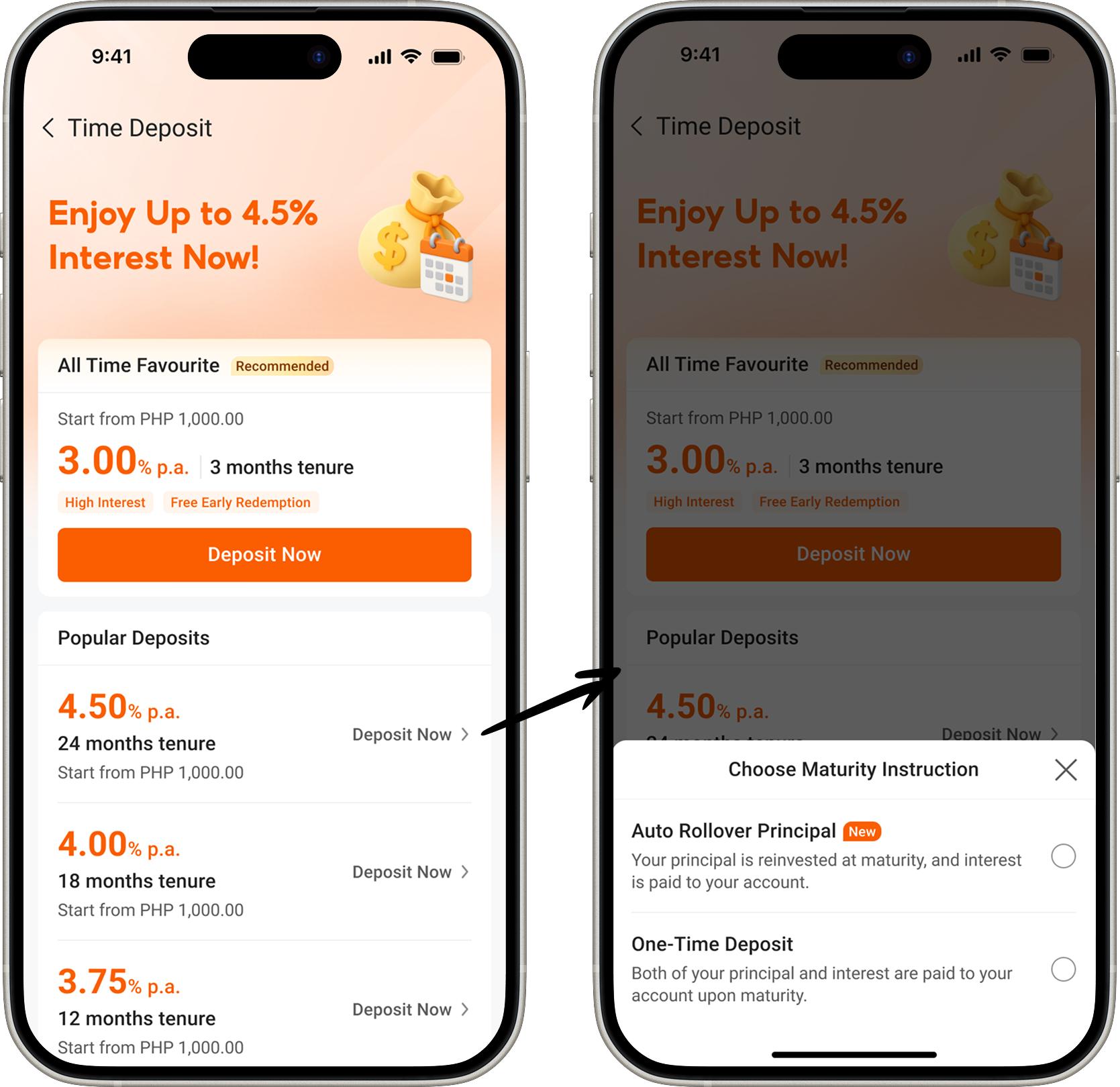

Option 3:

List + Bottom Sheet

We explored a bottom sheet to keep the page clean while giving enough space to explain each option clearly. It also creates a more intentional selection moment and scales well if we add more rollover options later.

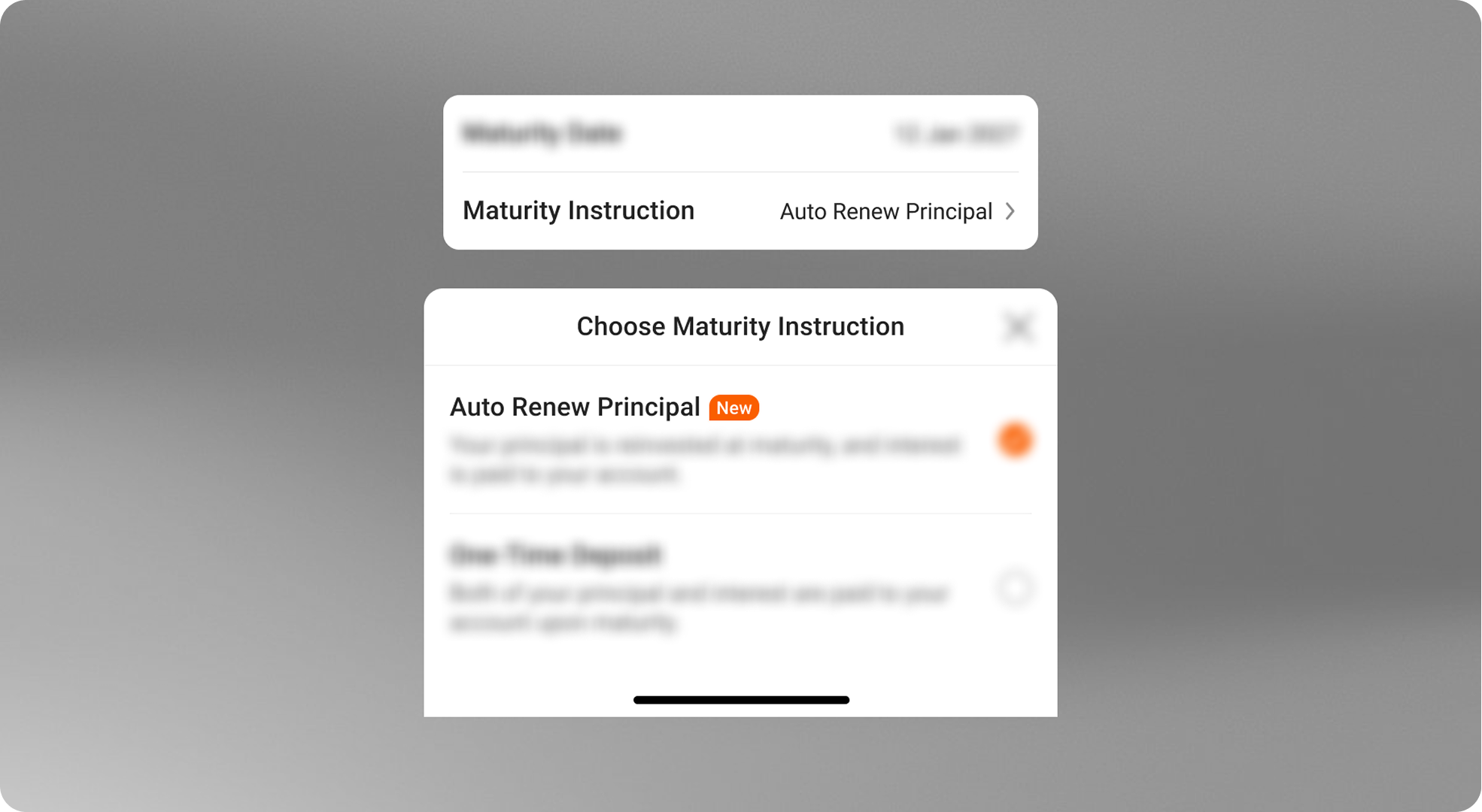

and... the decision was...

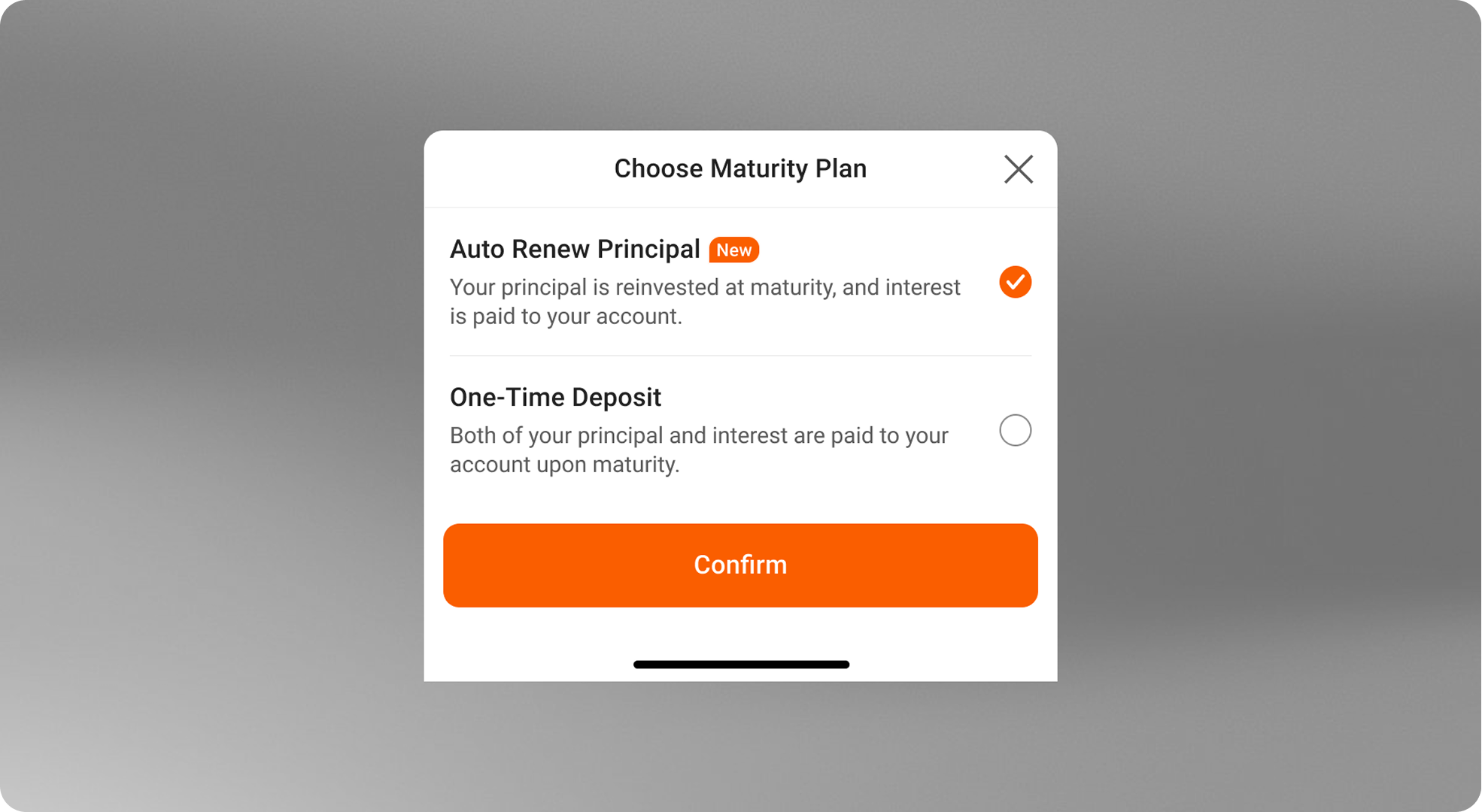

✅ We chose List + Bottom Sheet

This is because it gave the best balance of clarity and consent. It clearly frames rollover as a maturity "instruction," keeps the placement page clean, and adds only moderate friction (2 taps). Most importantly, the bottom sheet creates a pause-and-review moment, which improves decision quality and reduces accidental opt-ins.

Usability Testing

To validate clarity and consent quality for the maturity instruction setup, we partnered with the PH local UX team to run moderated sessions in Manila, Philippines.

Sample Size

10-15 users per key segment (aged 25-45 y.o.):

- First-time depositors (lower financial literacy)

- Repeat investors (rate-sensitive)

Localization & Language

- Prototypes fully localized into natural-sounding Tagalog (not just direct translation)

- Sessions moderated by native speakers to capture nuanced qualitative feedback

Task

Participants completed an end-to-end deposit setup, explained what would happen at maturity in their own words, and attempted to update their maturity instruction without help.

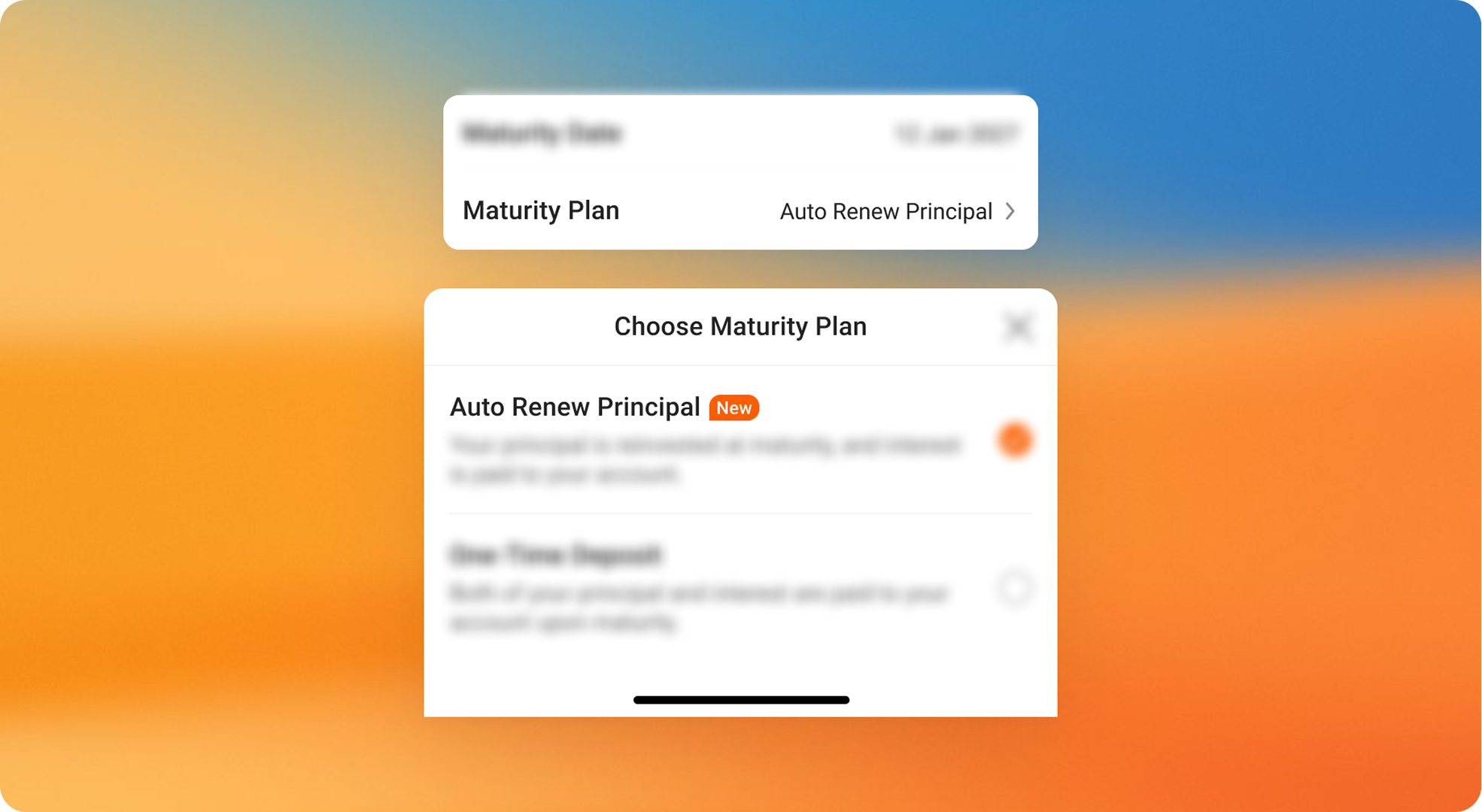

Iteration 1:

Simplified Banking Terminologies

Problem

Solution

Users didn't understand "Maturity Instructions" and "Rollover," and some thought they were complicated steps.

Renamed it to Maturity Plan and Auto Renew so the meaning is immediate and action-oriented.

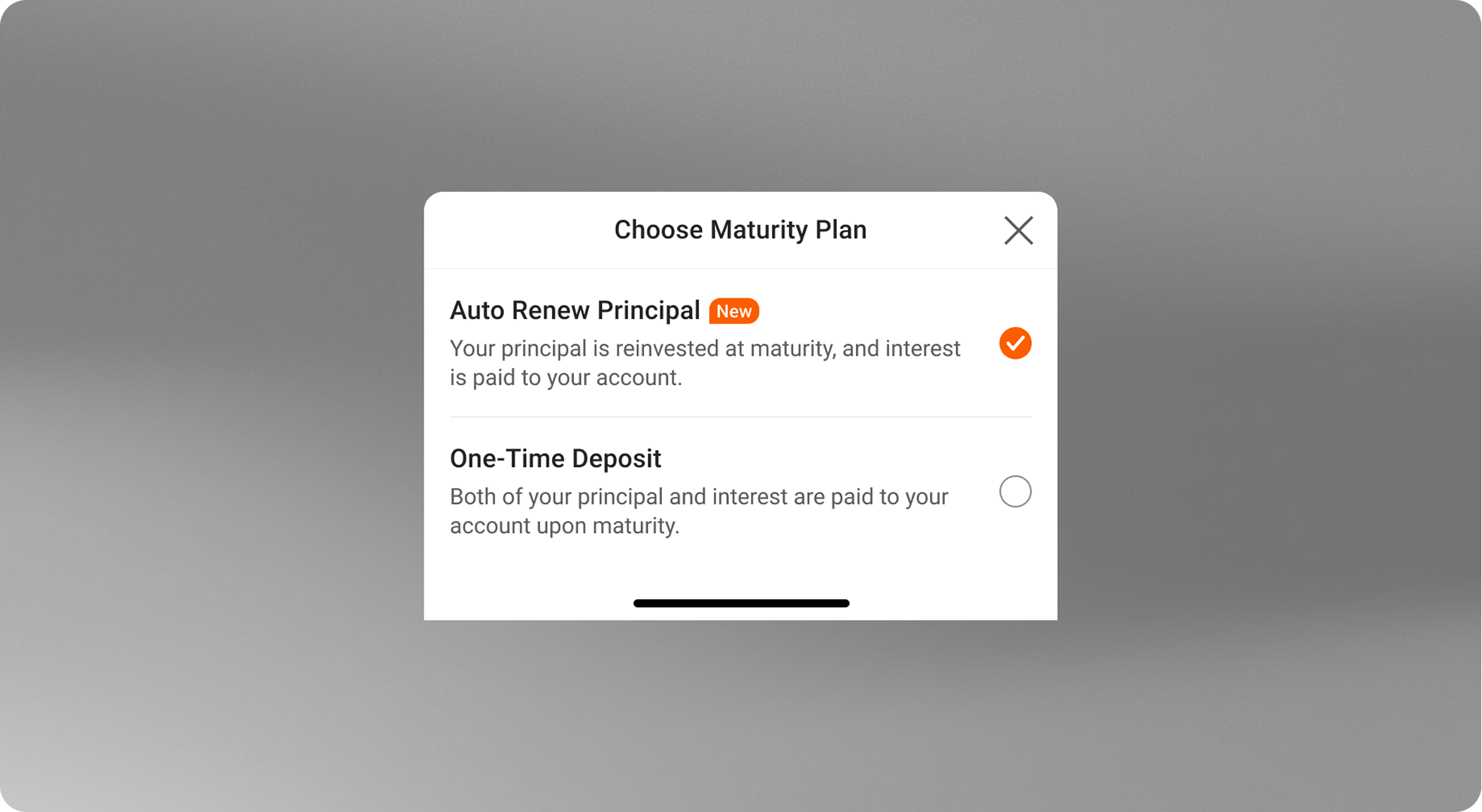

Iteration 2:

Prevented Accidental Inputs

Problem

Solution

Users accidentally triggered the selector while scrolling, then lost the sheet before they finished reading.

Added a two-step commit with a sticky "Confirm" button so the sheet stays open until they finalize.

Iteration 3:

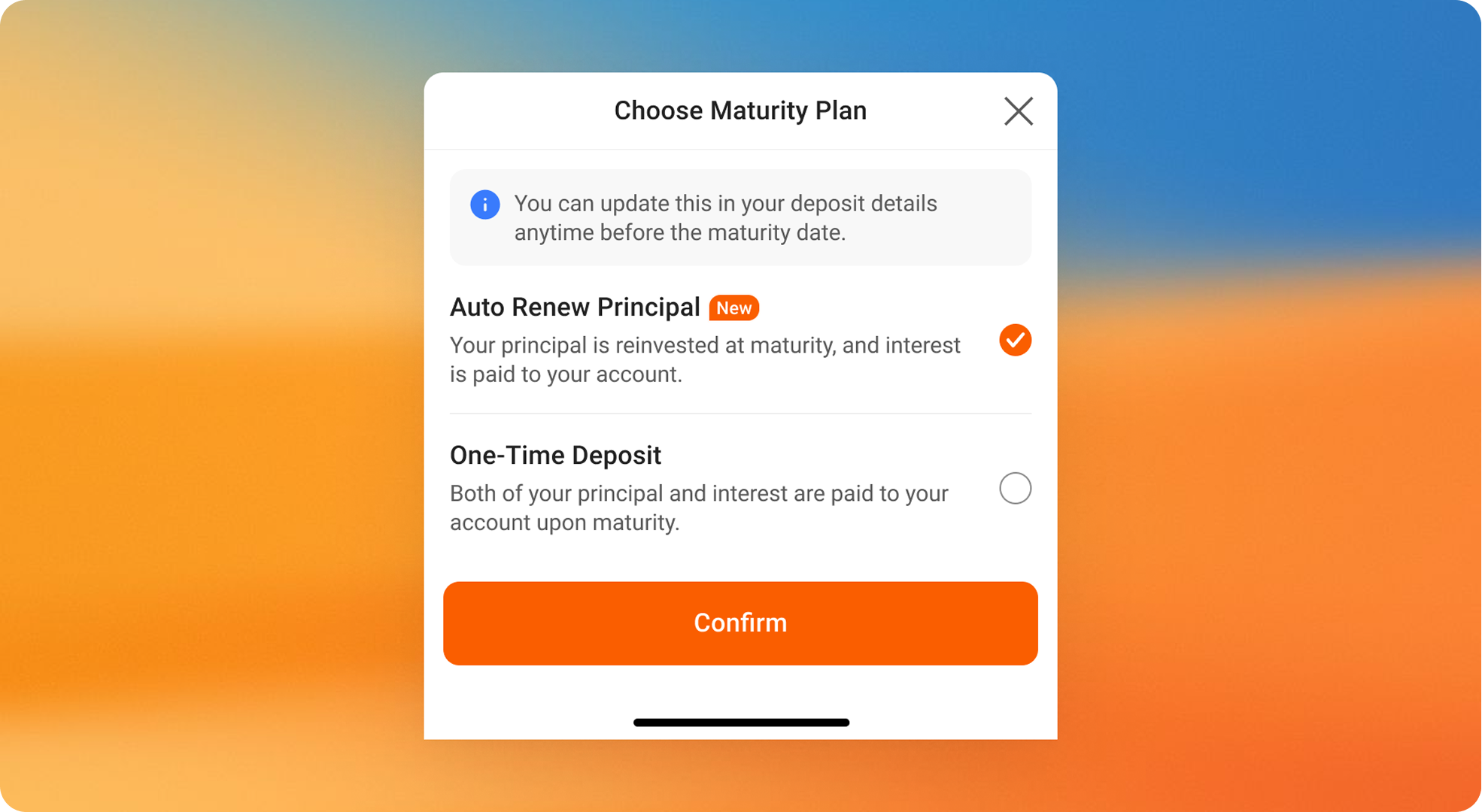

Clarifying The Changeability

Problem

Solution

Users hesitated to confirm because they feared they'd be locked in and couldn't access money later.

Made the escape hatch explicit up front by stating they can change the setting anytime before maturity.

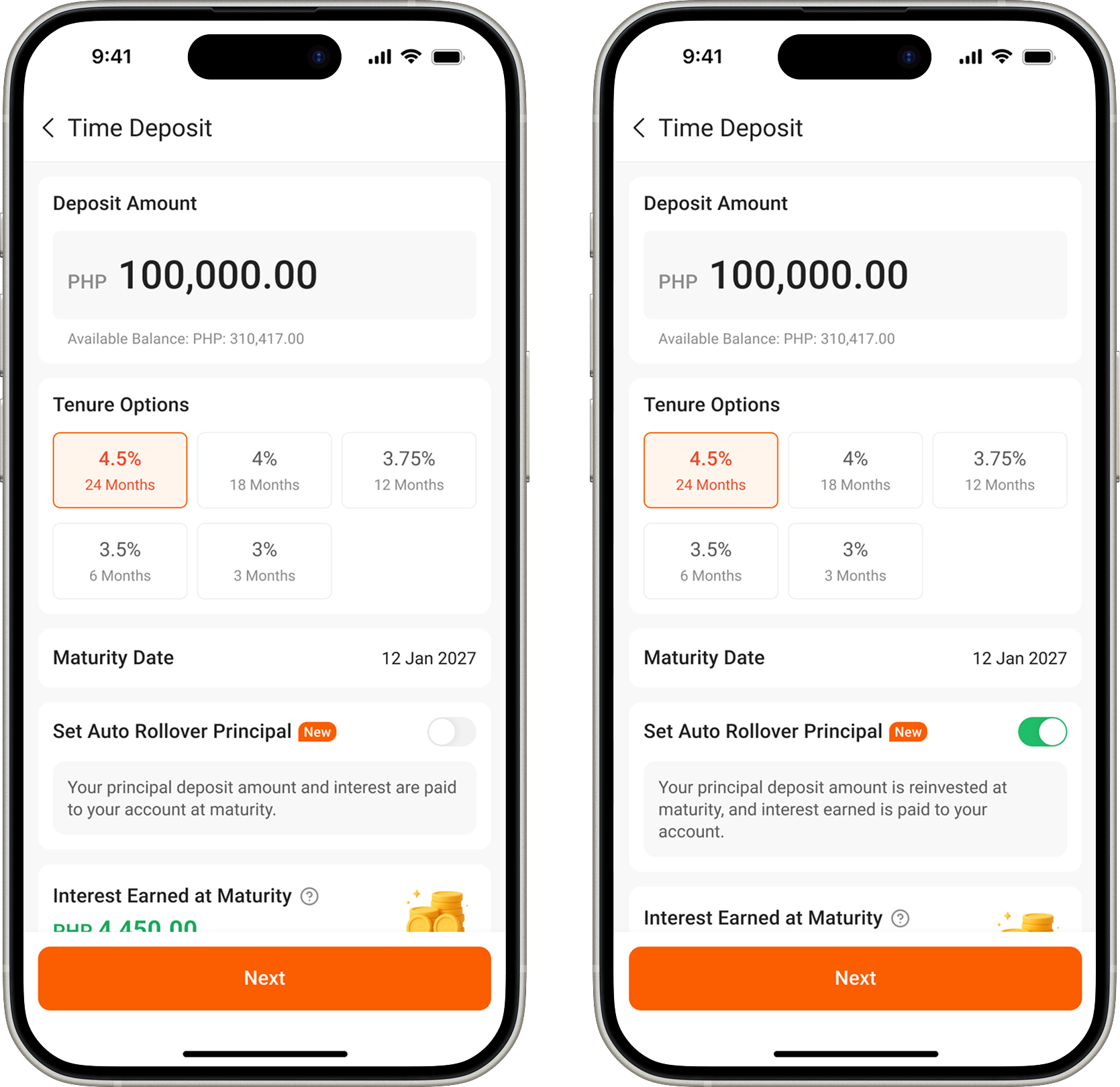

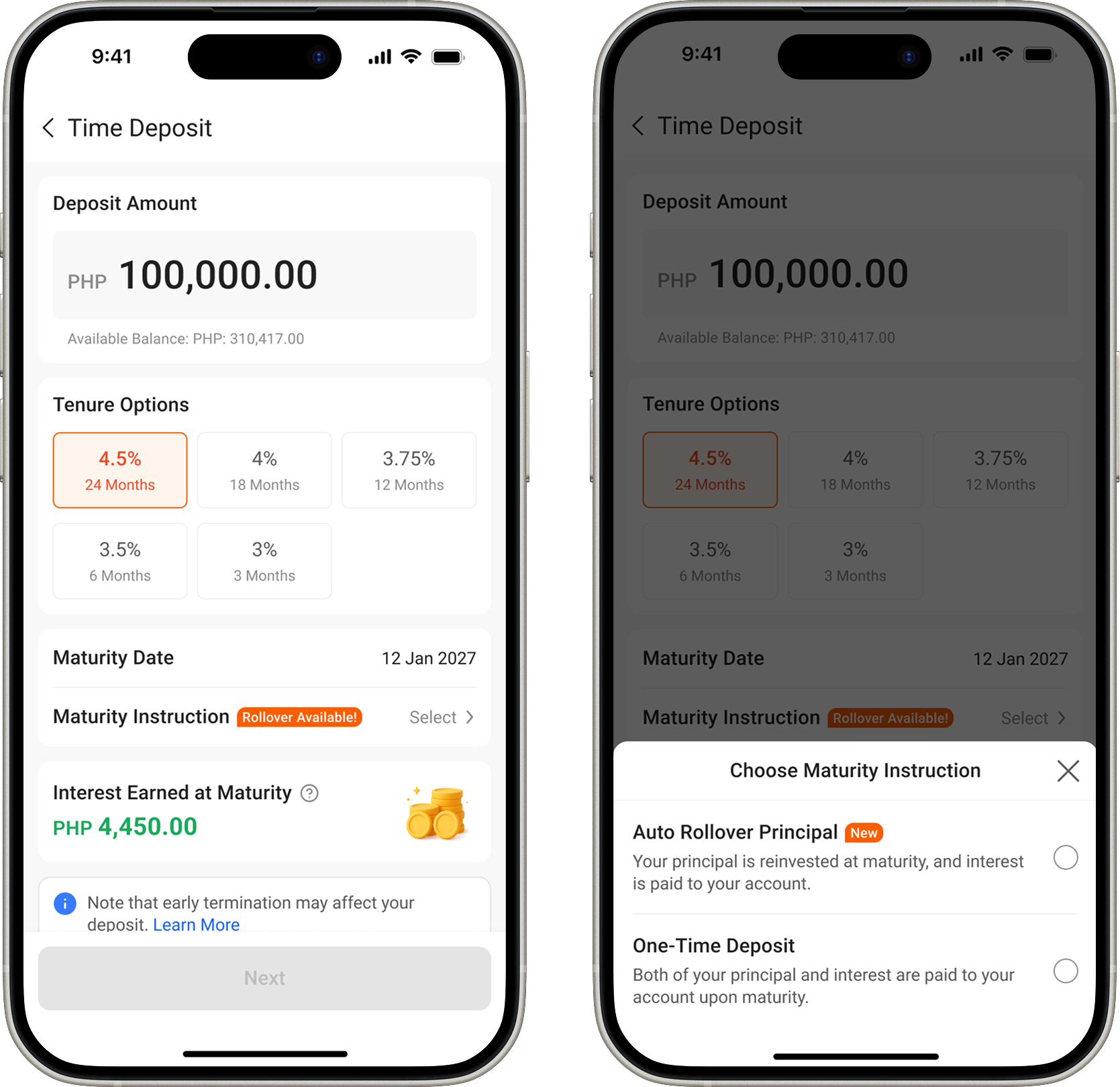

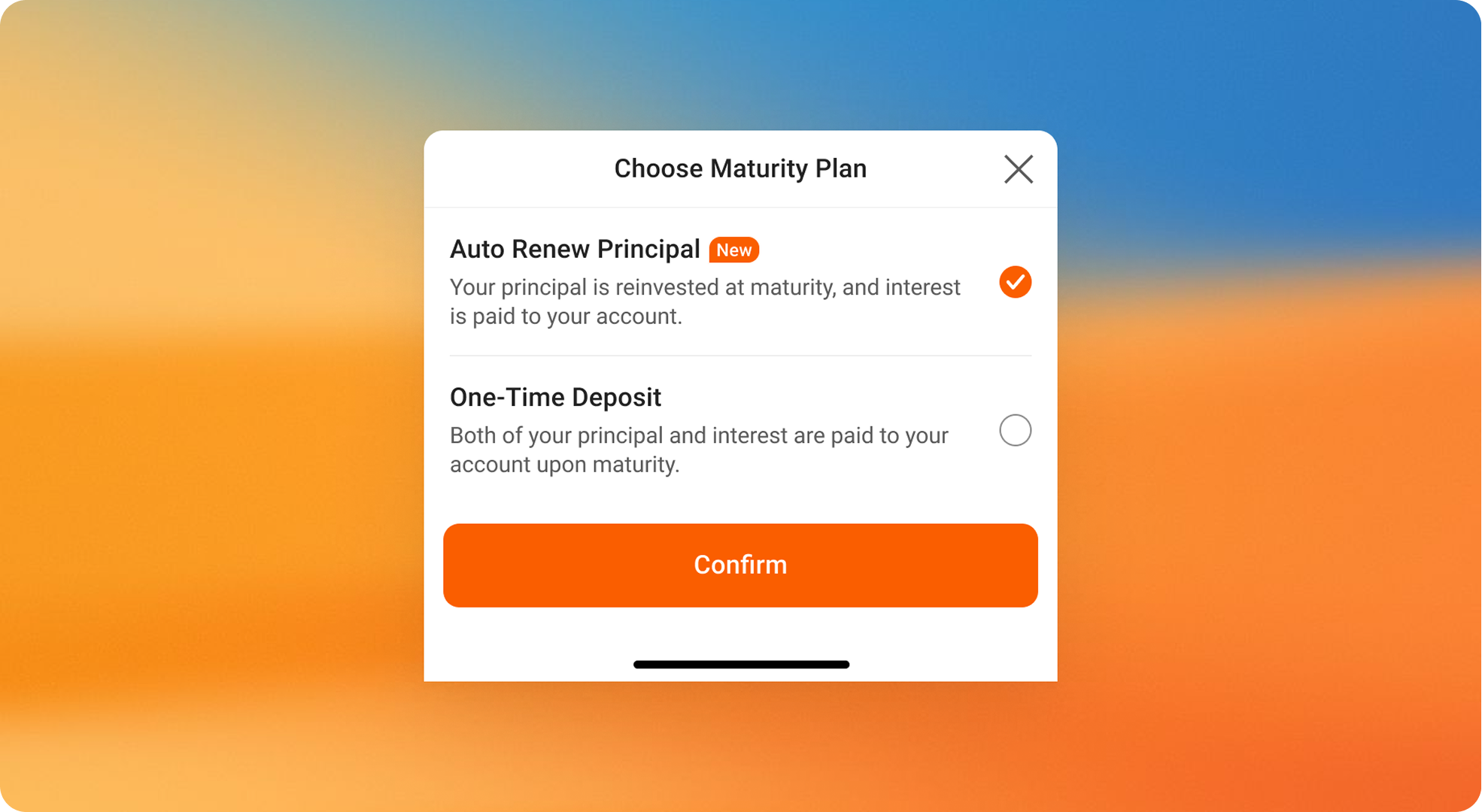

Final Design

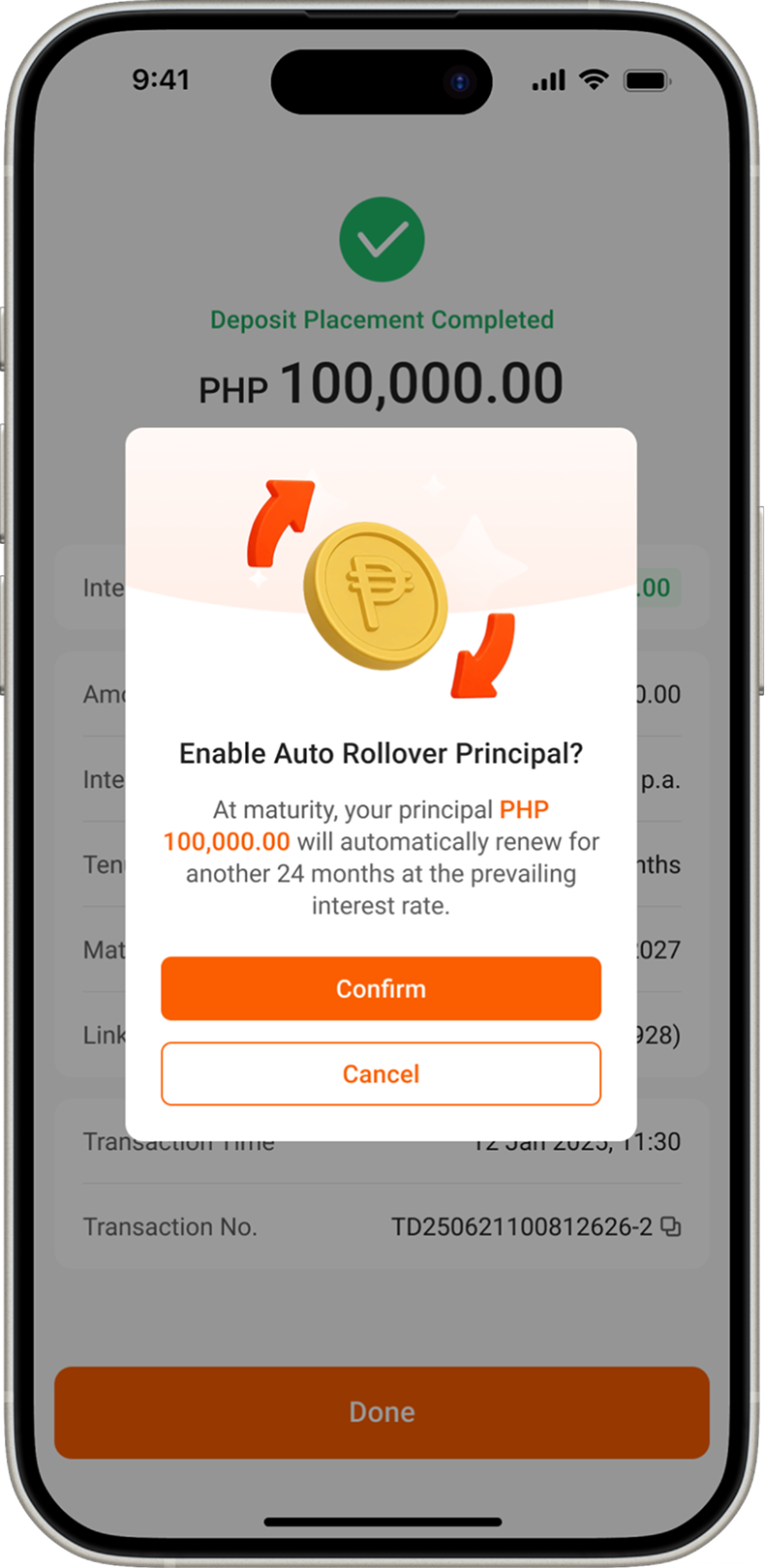

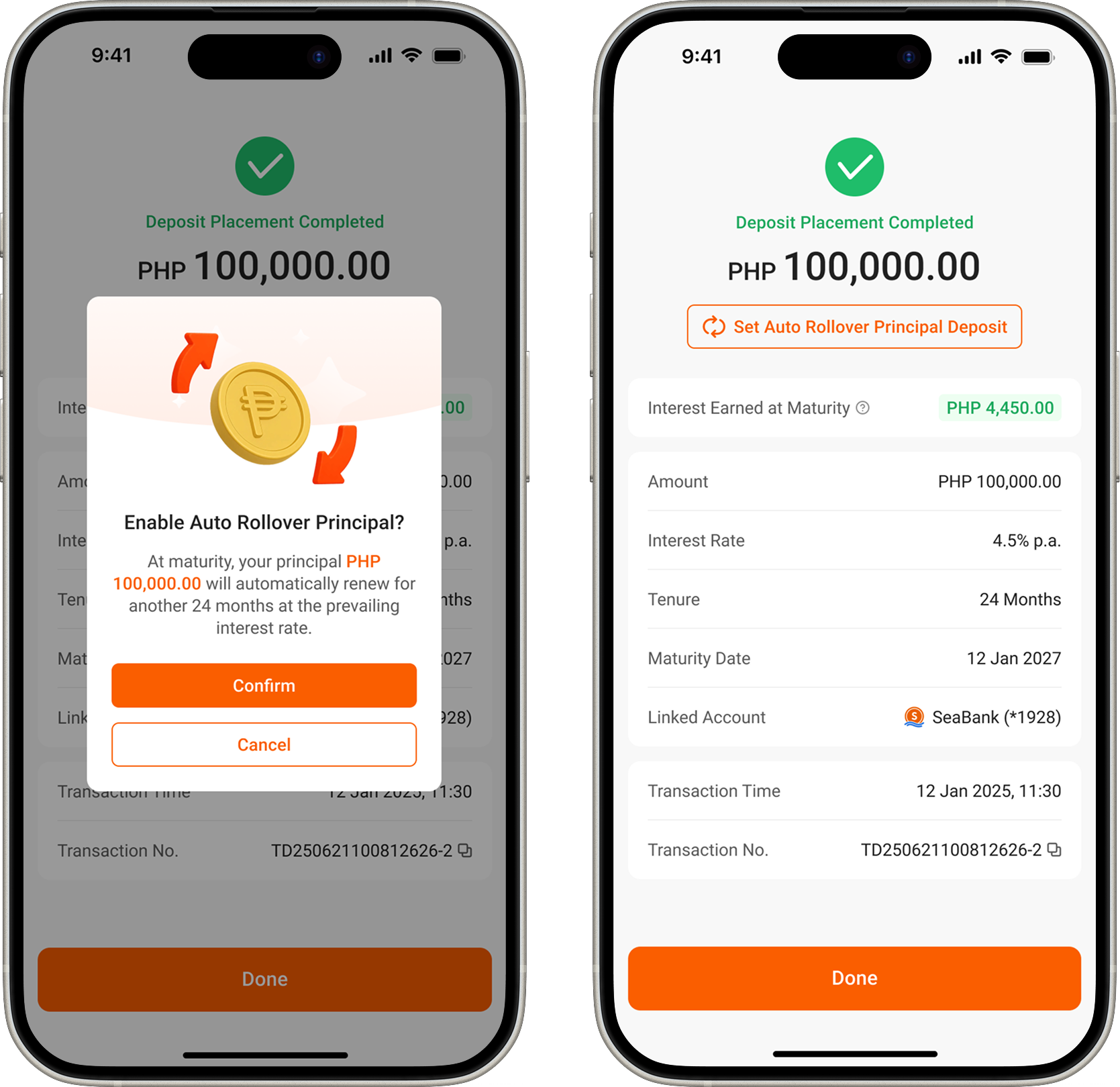

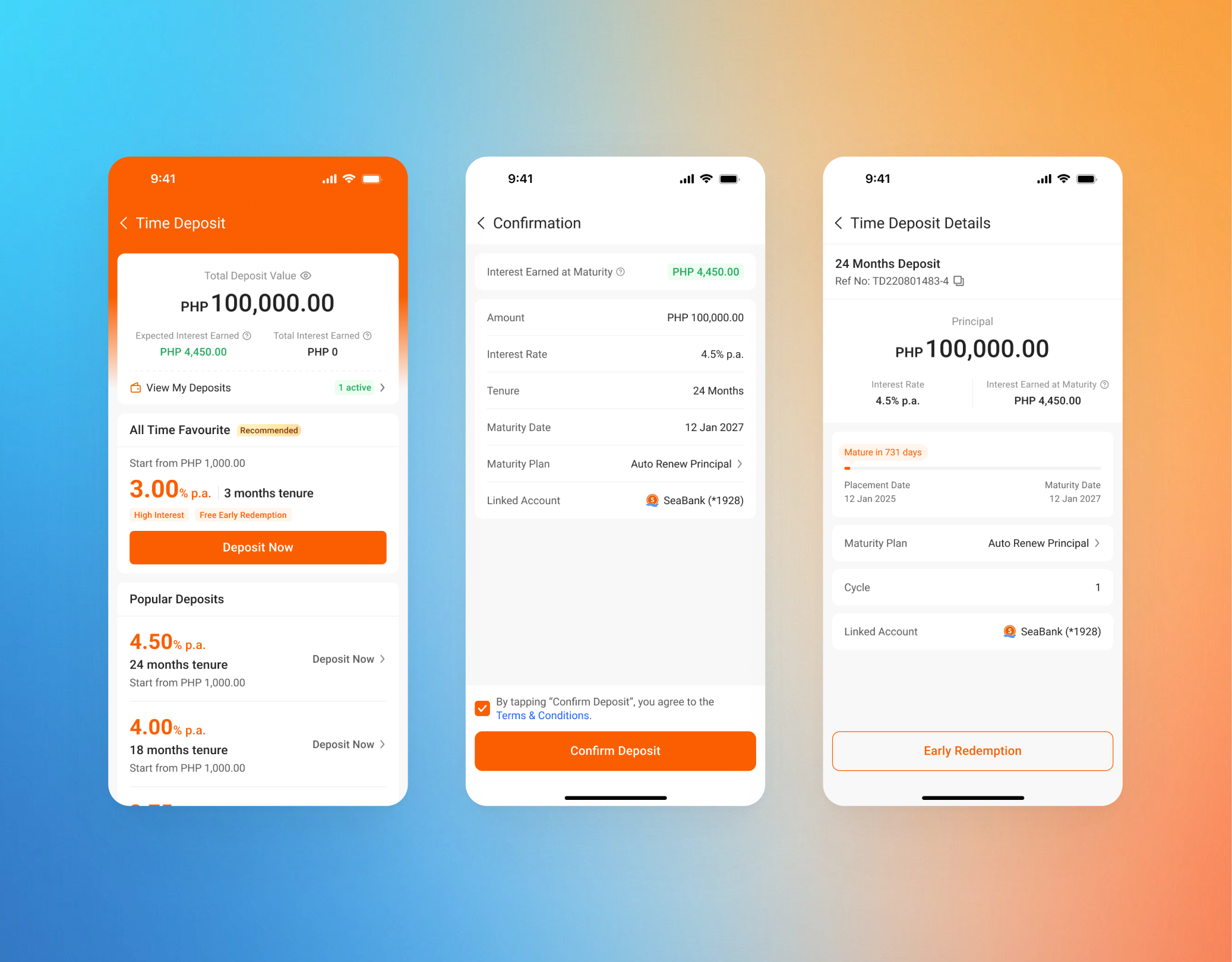

The final design adds a “Maturity Plan” in placement with a list + bottom sheet pattern. It keeps the flow lightweight, improves clarity, and ensures users confirm Auto Renew intentionally, with an easy way to change it before maturity.

Results & Impacts

Here's what we saw 4 months post-launch (Aug-Dec 2025)

22%

Auto-Rollover Adoption

Showing users understood & voluntarily enabled it in-flow.

27%

Post-Maturity Drop-Off (72H)

The % of matured TD balances not re-invested within 72 hours fell from 44% → 27%, shrinking the leakage window.

+9.7%

Portfolio Retention Volume

Day-14 retained principal improved by 9.7%, driven by fewer idle days before re-deposit.

Key Learnings

Timing shapes trust

Asking for decisions only when users have enough context prevents hesitation and unintended opt-ins.

Adoption isn't the goal

Real success is money staying invested after maturity, not just users turning a feature on.

Defaults must feel reversible

Rollover and maturity details are buried in account pages, with no clear countdown or visibility.

Use plain words

Plain and straightforward copy not only builds trust but also significantly reduces confusion among users.

Future Improvements

Dynamic Rate Messaging

Introduce "Rate Alerts" so users are notified if the auto-renew rate drops significantly compared to their initial term.

Goal-Based Deposit

Let users set a goal with their time deposit to increase motivation and encourage them to keep their money in our platform.

Compounding Growth

Offer a "Principal + Interest" auto-renewal option, maximizing compounding benefits for users and AUM for the bank.